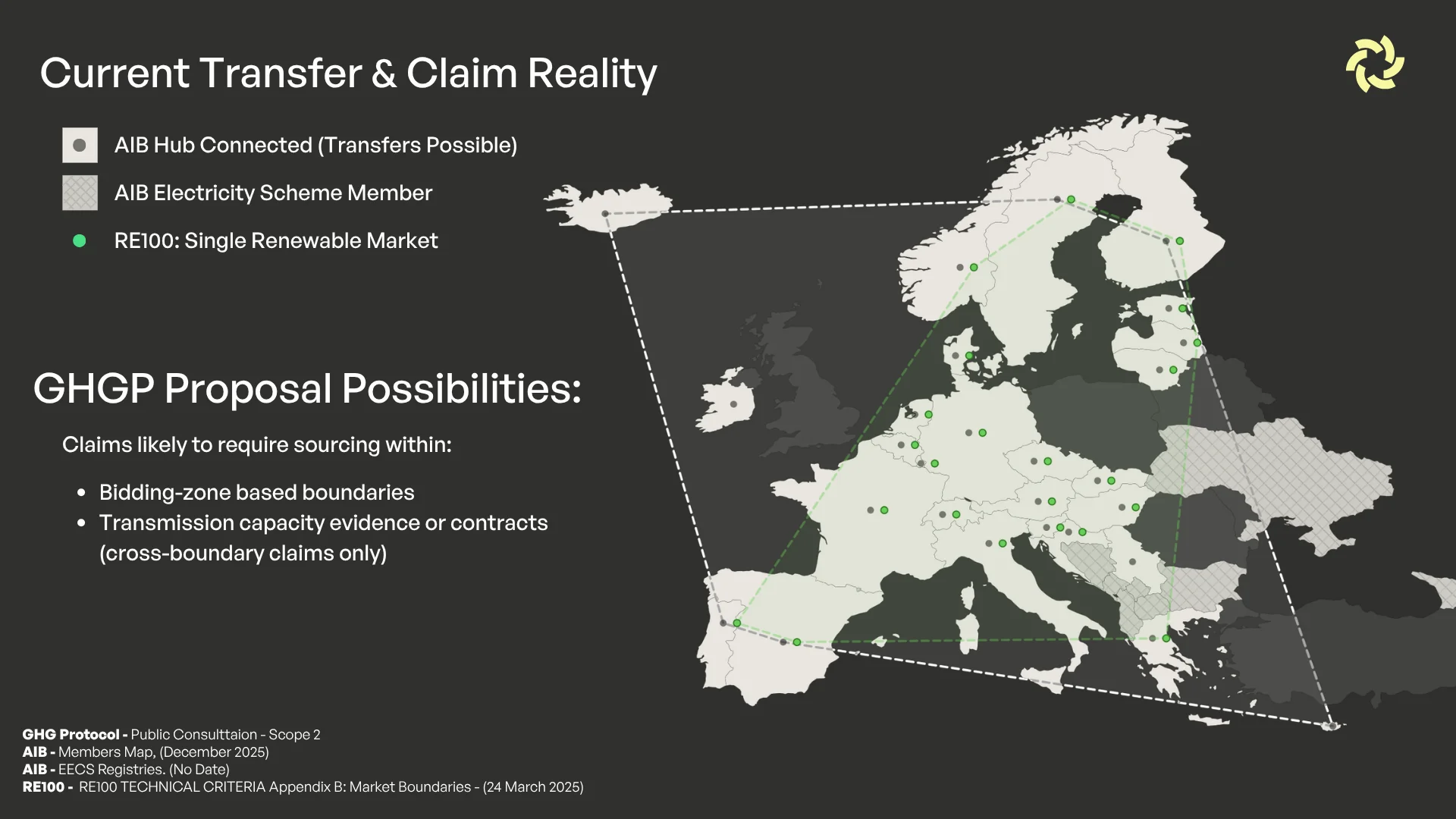

How Will the GHG Protocol Changes Impact Geographic Matching in Europe?

The GHG Protocol's draft scope 2 revisions, whilst not confirmed, would, if adopted, enact a thorough, structural shift in how companies source renewable energy certificates across borders.

The sourcing of correct certificates for credible claims under various private reporting frameworks carries truly outsized consequences - so at Soldera , we’re laying the groundwork for European buyers to traverse ever-tightening trends in geographic deliverability rules from within our platform.

What changes are predicted?

Based on what the consultation document actually says regarding the GHGP, the most likely changes to credible sourcing are as follows (within Europe)

- Bidding-zone based boundaries

- Transmission capacity evidence or contracts (cross-boundary claims only)

What will this mean in practice?

Under current practices, a company that’s operating in Germany or the Netherlands can readily purchase Guarantees of Origin from Icelandic producers. Whilst not eligible as per RE100 market boundaries for a RE100 credible claim, the current GHG Protocol ‘same market’ quality criterion has, in practice, allowed broader cross-border matching than the draft deliverability rules would require. Draft revisions would curtail this all-too-familiar arrangement.

Moreover, non-island production sites, e.g those from Norway, may see changes as well. Deliverability requirements are likely to mandate that certificates originate from generation capable of physically delivering electricity to the consuming load within defined, territorial market boundaries. Sourcing a Nordic GO to cover a Dutch factory would only qualify where physical transfer within the approved boundary can be demonstrated, and that particular demonstration is quite difficult in practice.

Concentrating procurement pressure onto local and sub-regional GO supplies is the direct, mechanical result when these changes are implemented. Regions that have long exported cheap, abundant surplus certificates would see those instruments lose eligibility for buyers outside the new boundaries. Deficit countries, meanwhile, would face hard-pressed supply and elevated prices. GO markets have shown this emergent dynamic in early form; as volumes with provenance from surplus ( net exporter ) regions typically remain reasonably cheap, while countries where geographic constraints have been imposed, as with UK REGOs after Brexit, can see prices in their market spiking sharply under constrained conditions. Squeezing this trend further with changes to reporting eligibility is a positive step for producer incentives, leaving buyers competing for an ever-diminishing pool of qualifying generation in exactly the markets where ravenous demand is highest.

What risk do underprepared buyers face?

Changes are coming whether you’re prepared or not. Here sits the often-overlooked, and really quite consequential risk.

- Currently - Any consumption that is not covered by qualifying instruments under the GHG protocol must be reported using residual mix emission factors for the relevant market boundary and time interval. Companies can fall back to grid-average factors where residual mix isn't available

- Draft Proposal - No more fallbacks. Where no residual mix data exists for a given boundary, the draft requires a fossil-based default: the peculiar and punitive emission factor of fossil generation alone, with grid-average figures (those used in location based reporting ) will no longer be permitted as fall-back figures.

Securing these qualifying, geographically-matched certificates from correct market boundaries is therefore a highly-pressing focus for buyers, because not only is geographic tightening is driving concern here, but the likelihood of worsened reporting numbers (via the residual mix ) is going up. A company with comprehensive annual coverage today could well find substantial renewable European load under current methods reclassified as non-renewable purely because sourcing strategies haven’t adapted to newly drawn lines and because location-based factors won’t be able to ‘save the day’ anymore. In short: the walls are closing in. Tracking this across dozens of markets with disparate registry capabilities and staggered reform timelines; compounds what begins as a procurement problem into a genuinely sprawling data and operations problem.

How can buyers prepare in advance?

Any eventual revision will reward organisations that can source verified, in-boundary certificates and document cancellation with precision across jurisdictions.

Platforms like Soldera , which connect to 30+ EAC registries where available and provide verified cancellation statements with export-ready documentation, offer a very practical route to maintaining certificate eligibility as geographic matching rules truly tighten across Europe. Stay prepared!

You're halfway there...

Sign up free to keep reading immediately and get Soldera's EAC market research, price updates, quarterly outlooks and renewable compliance insights direct to your inbox.

Schedule a 20-minute demo to find out if Soldera is right for you.